Blockchain - An Overview of The Trillion Dollar Market

In 2011, Marc Andreseen prophetically stated that software was eating the world. To date, blockchain adoption has been faster than that of the internet.

Blockchain is eating the world. It was in 2011 that Marc Andreseen prophetically stated that software was eating the world. To date, blockchain adoption has been faster than that of the internet.

When trying to understand the magnitude of the shift that is occurring, there is a temptation to resort to traditional market sizing techniques.

Healthcare + blockchain. Finance + blockchain. Music + blockchain. The list goes on...

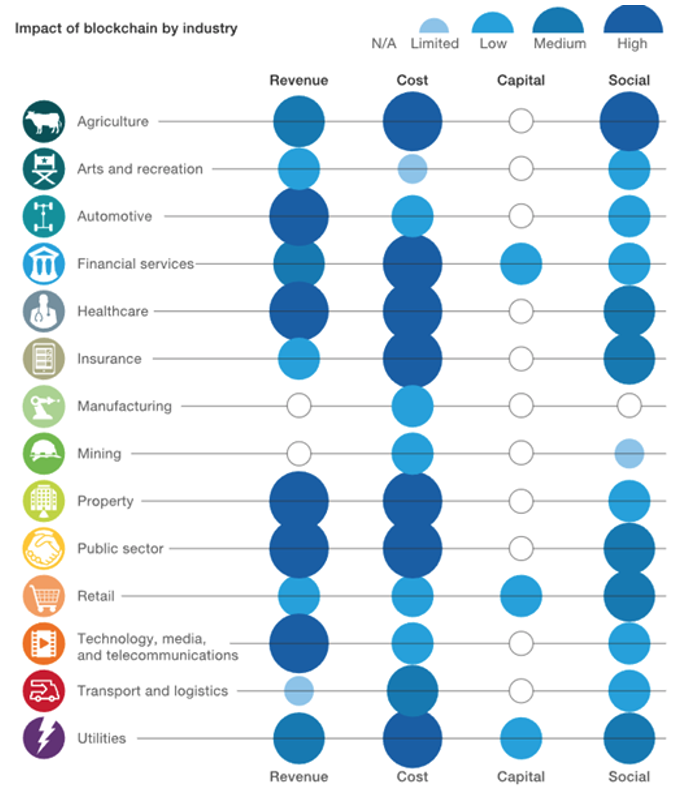

Source: McKinsey & Company

At Aura Ventures, we have found this to be unhelpful as blockchain will change every industry in some capacity as well as create new ones. Instead, we chose to focus on the different layers of the blockchain onion and the use cases that peel off at each layer. This approach is far more ecosystem centric and clearly separates enterprise adoption against startup activity.

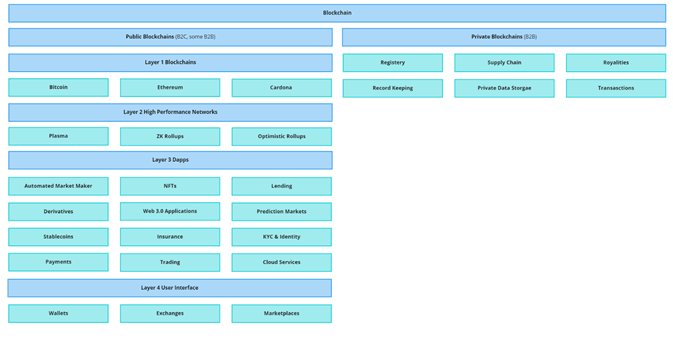

Our market map looks this:

Where is the opportunity in this labyrinth of use cases?

Before we explore that, we need to understand some key terms and the structure of the ecosystem.

Private and public blockchains are very different. Public blockchains that we know and love, include Bitcoin, Ethereum and basically any protocol that you can buy and sell on an exchange. Many people around the world own the network - it is decentralised by design. Contrast this to a private blockchain in which the infrastructure is owned by a central authority and only authorised participants can add to the blockchain.

Private blockchains

Private blockchains get little attention, but we believe they are generating considerable real-world value. Whilst the promise of offering maximal efficiency for large enterprises as a fundamentally new data structure is not appealing to the public, it is world-changing. Not in its promise of a new system but in making the existing one incrementally more efficient.

There are a few use cases across industries that the private blockchain excels in - registry, supply chain tracking, royalties, secure data storage and some types of transactions.

For example, the Danish shipping conglomerate - A.P Moller-Maersk is digitising the world’s supply chain information for container ships. With the help of IBM’s private blockchain, they have already onboarded roughly 50% of container ships in the world. Imagine if you could trace where each part of the car you bought came from - tyres from Denmark, steel from Germany and leather from Italy.

Carrefour, a French supermarket, is doing exactly that for food by tracing more than 30 of its product lines on a private blockchain. Consumers can track produce such as eggs from farm to plate. These use cases leverage all the promises of blockchain without being restricted by the scalability issues of a public blockchain.

Closer to home, our portfolio company, Lygon, uses a private blockchain to digitise bank guarantees bringing both speed and trust to an archaic process that wastes 4 million pieces of paper per year.

In 2019, analysts found that private blockchains accounted for nearly half of the value capture in the blockchain market. While the pendulum has no doubt shifted to public blockchains, we believe it will shift back.

Private blockchains with enterprise adoption do not face the chicken-and-egg problem common to most two-sided platforms. Large enterprises can onboard one side rapidly to the platform and instantly benefit from the advantages of the new technology without the limitations of scalability and speed. Just look at Walmart ‘requesting’ its thousands of suppliers to start using its private blockchain to track the supply chain.

Public blockchains

For all their limitations, public blockchains are magical.

A public blockchain is an immutable ledger that each node has a copy of in a decentralised network. It allows computers that do not trust each other to work together to form a powerful supercomputer that is trustworthy and reliable.

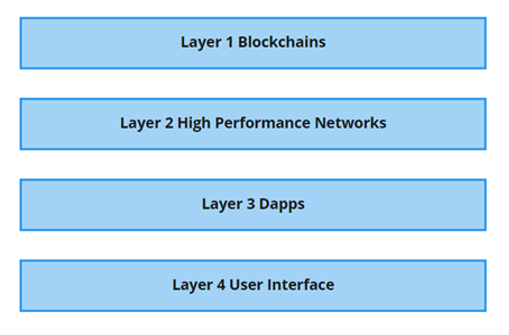

There are four fundamental layers to the public blockchain ecosystem:

Layer one (L1) is the underlying blockchain itself. Think Bitcoin, Ethereum & Cardona.

Layer two (L2), is a third-party integration/network designed to improve the performance of the underlying blockchain. Think Starkware, Immutable X & the Lightning Network.

Layer three (L3) are smart contracts that run on top of these networks & protocols (called decentralised applications or Dapps). Think Compound, Uniswap & Synthetix.

Finally, Layer four (L4), is how people connect and interact with these Dapps and blockchains (the user interface layer). Think Coinbase, Binance & Metamask.

Note: We will be deconstructing these layers further in a future article.

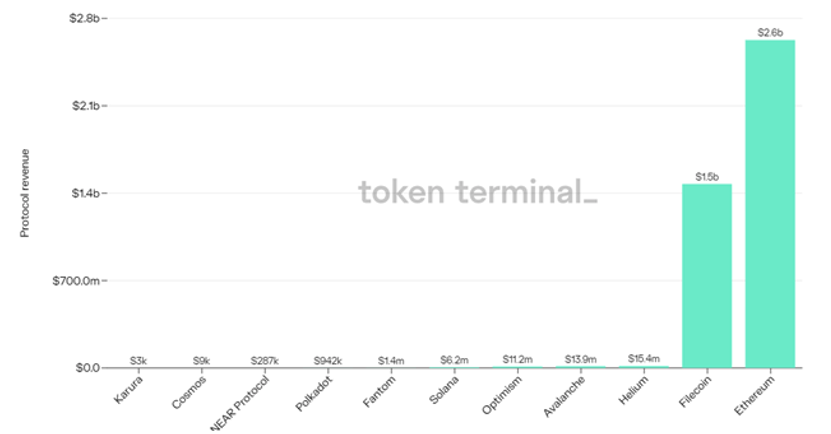

For a long time, most of the value has been concentrated around Layer 1 blockchains. Speculation has made it very profitable to be the holder of a cryptocurrency that goes to the moon.

Most of these coins are trading at multiples that far exceed the underlying revenues generated.

Cosmos made $9k in the last twelve months from protocol revenue, its market cap is USD 8.5B as of late 2021. Now some might argue that it is a good sign if an L1 protocol generates such little revenue for the protocol as it is not meant to be a profit-seeking company but a public utility.

So that begs the question, where does genuine, non-speculative value come from in crypto land?

As the system matures, we believe greater value will be generated from L2 & L3.

This has already been seen with L2 scaling solutions raising some very large rounds.

Some exciting things are happening in L3 Dapps, with Defi being the most mature part of the ecosystem.

Take the Aussie company, Synthetix as an example. It allows you to trade derivatives of currencies & even equities in a completely decentralised matter. You could trade Gold for Apple without any need for a bookmaker as the protocol relies on a peer-to-peer liquidity pool.

Blockchain is taking its first bite of the multi-trillion dollar derivatives market.

It’s little surprise that over USD 100 billion is locked in Defi applications as of late 2021. The financial sector has been a great on-ramp for the technology. Early adopters are technologically savvy and enjoy the many creative financial products on offer. From a technology perspective, executable smart contracts lend themselves perfectly to the financial industry, a historically opaque industry with lots of complex financial products based on programmable rules is ripe is perfect for disruption.

But there is more going on outside of Defi. Non-fungible tokens (NFTs) are establishing new primitives that combine art, gaming and culture. Audius is a music streaming platform that is built on the blockchain and offers far higher royalties for artists and better quality music for listeners. Helium is a decentralised wireless infrastructure offering coverage for billions of devices at a fraction of the cost of incumbent infrastructure/services.

Where to from here?

The adage is as old as time, in a gold rush sell pick axes. Every investor initially wants to support the infrastructure layer of the ecosystem as opposed to more speculative crypto consumer companies (Soldate is one of them). Much of the early work supporting protocols and L2 scaling solutions has been done which means there is still more infrastructure to be built on top of that.

At Aura Ventures, we believe in products that people love. As an investment thesis, this translates to understanding where the advantages of blockchain are indisputable and investing in companies that provide a 10x better consumer experience – infrastructure layer or not.

Important information

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Group and related entities and is only for information and general news purposes. It does not constitute an offer or invitation of any sort in any jurisdiction. Moreover, the information in this document will not affect Aura Group’s investment strategy for any funds in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Aura Group makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this information. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. You should not construe any such information or any material, as legal, tax, investment, financial, or other advice. This information is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The information may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This information is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in any way.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia.