If Open AI’s GPT-3 were to analyse all venture capitalist’s investment memos, medium articles and tweets, it would probably generate something like this:

“Flywheels lead to network effects which generate CAC/LTV for Patagonia multiples of 5000%. Is there revenue?”

Network effects are commonplace in the VC lexicon. Just like lexicon, it is a word that can be needlessly complex. To simplify the phrase, I would like to explore examples of network effects in some of the best Aussie start-ups. Hopefully by the end of reading this article you will have a better understanding of what they are, the different types and some practical examples.

What are network effects?

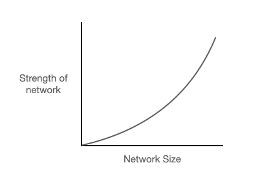

Network effects are when every new user to the network adds more value to existing users. Mathematically, a network effect can be represented as V=N². Where V is defined as network strength and N is the size of the network.

Visually, it looks like this:

Basically, as more people use the product it becomes better by virtue of more people using it. The clearest example of a network effect is a social network. As more people use LinkedIn, the more valuable LinkedIn becomes to it’s existing users. There are more people to connect with and message prospective employers or employees. More users leads to a better experience which leads to more users. This is a flywheel.

But what’s more important to focus on is the value that accrues to existing users from simply being a part of the network. Network strength alone becomes one of the greatest aspects of the product/service and is exceedingly hard to compete with for new entrants. Amazon has obtained network effects with it’s marketplace, Bitcoin with it’s protocol and Microsoft with it’s operating system. Network effects are more about defensibility than growth.

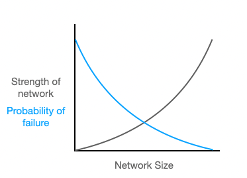

While most of the attention is on network strength, it’s often neglected what else is happening. After a network size reaches critical mass, the business is becoming exponentially less likely to fail.

Although amazing businesses can still have no network effects and grow exponentially. The catch is that their probability of failure does not decrease exponentially. In other words, these companies are beholden to product innovation, brand and scale to remain ahead of the competition. The moment they start to falter on these, is the moment their business fails. It is why companies like Evernote can amass a huge loyal user base and then lose it in a matter of years. There were no network effects to retain users, the product did not get more valuable by virtue of more people using it.

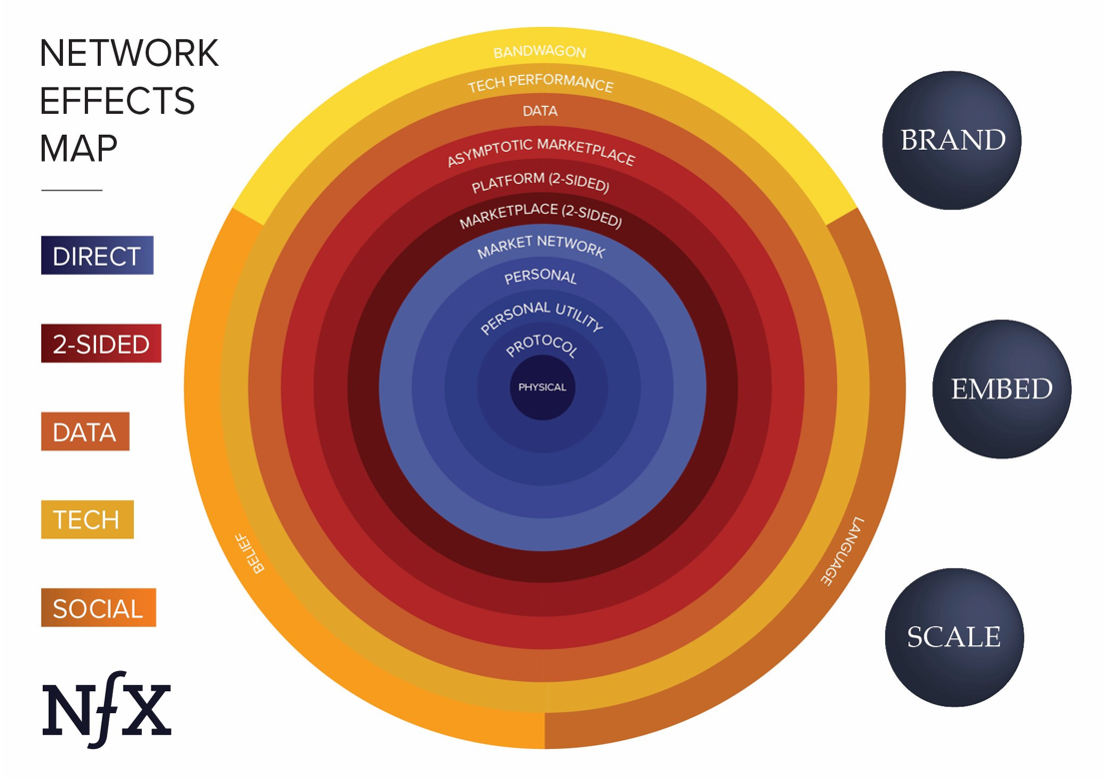

In practice, there are many different types of network effects each with a different type of function. NfX has identified thirteen but I will focus on a select few. The network effects get incrementally weaker for each layer away from the centre of the circle. For the above examples, Bitcoin is a protocol NfX, LinkedIn is a personal NfX and Amazon is a marketplace NfX.

Hopefully, by exploring some examples and the practical application of network effects, the concept will become clearer. Today we will look at:

1. Airtasker

2. Redbubble

3. Canva

4. Linktree

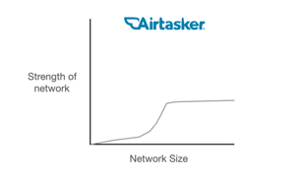

Airtasker

Airtasker is an Aussie marketplace with over two million users and was valued a market cap of at AUD 450 million as at 30 June 2021 (ART.ASX). It is a two-sided marketplace that connects customers who want an everyday task completed (demand) with people looking to do odd jobs for cash (supply). Does it have network effects?

Short answer — yes! Marketplaces have strong network effects, which is why they are so hard to create. Each new user looking to post a task directly adds value to the supply side by providing the opportunity for more work. Conversely, each new person looking to do a job adds value to the demand side by driving down prices. These are called cross-side network effects. So most people will likely go to the largest marketplace because there is already supply and demand. It’s where all the buyers and sellers are. It can get a little bit more complicated with things like same-side network effects, but you can read more about them here.

The network effects are so strong in marketplaces that they lead to natural monopolies, it’s why Amazon and eBay have long outlived the dot com bust. But why is Airtasker’s not as strong?

Airtasker has an asymptotic network effect because there is a point where each new user does not actually provide any additional value for existing users. Put simply, if I can already get my broken bike fixed for $10, adding one million handy Australians to the website will be of no extra value to either of us. The service is already priced at it’s lowest market rate and there is already enough people willing to do it. It doesn’t benefit the customer to have lots of people who can do the same job for the same price. The same phenomena can be observed in ride-sharing. There is a liquidity point where there are enough drivers to get a lift within 2–3 minutes for a reasonable price in most major cities. Past this point, the network effect becomes asymptotic. This is what A16z calls a ‘commoditised marketplace’ whereby the product is not differentiated as it is a low skill task that anyone could do. While there is still a network effect, it is not as strong because the marketplace reaches a point where additional supply or demand provides no additional value.

Note: This is why Airtasker is trying to expand into things like design (more differentiated, stronger network effects).

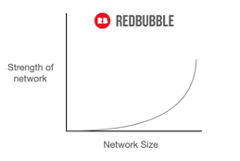

Redbubble

Redbubble (RBL.ASX) has a market cap closer to AUD 1 billion (as at 30 June 2021) and are also a two-sided marketplace. However, I have included them because they are a good counter example to Airtasker. Redbubble is a differentiated marketplace. They connect designers who have made uniquely designed products (supply) with consumers (demand). Does it have network effects?

Yes! It has even stronger network effects.

Every design on the platform is different be it shirt, phone case or apron. This means that every new designer that joins the platform, improves the experience for the demand side by providing greater choice. So there is no asymptote as there was before. It’s business becomes more defensible as it’s network grows.

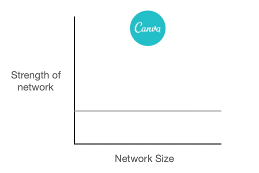

Canva

Canva is one of the best companies in Australia, valued well over USD 15 billion (source: Canva, April 2021) with more than 55 million active users. It has a product that consumers love and has transformed the design industry from an archaic user experience to a delightful one. But… Does it have a network effects?

Not yet! This one seems the most counterintuitive, as Canva is one of the most successful Australian startups. But the strength of Canva’s network does not vary with network size. For each additional user to Canva, there is no additional benefit to existing users. If there were 20 million users added to Canva overnight, it would provide zero marginal benefit to its existing user base. More is not better.

What are the implications?

It means Canva relies on other superpowers to defend its place in the market.

Canva benefits from economies of scale because the fixed cost to produce design assets can then be distributed to millions of users. There are also switching costs if all your designs are on one platform. But Canva primarily competes by having the best product, which this has led to amazing growth. But product innovation does not necessarily lead to a defensible position in the long term.

It begs the question of how Canva could benefit from network effects? If users could design templates for other users, this would lead to considerable network effects. Content could be curated by moderators and designed by power users, increasing the value for everyone as the user base grows.

Update: Canva does this! Admittedly they did it before the article, it’s called Canva Creators, see here.

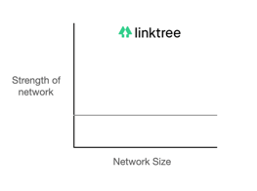

Linktree

Linktree raised USD 45 million1 in early 2021 and invented the ‘link in bio’ market. Their product enables content creators to centralise their digital existence by putting all of their websites, social media channels and campaigns in one link. But… Does it have network effects?

No! I included Linktree to show the difference between viral effects and network effects. Viral effects are when you get your existing customers to acquire more customers for free. It is all about growth as opposed to defensibility. Each time an influencer puts a Linktree link in their bio, it acts as a viral sales engine. Their fans see the link and then use the link and then their fans see the link… This is also a flywheel but a very different one. If you want to read more on the difference, here is a great article.

All of these are great businesses and all for different reasons. I hope you have a better understanding of network effects, demystifying the VC jargon. I would also love to hear more about what companies you think have network effects or businesses that you are building. Please feel free to reach out at sean.stuart@aura.co

If you would like to read further on the topic here are some great resources below.

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Group and related entities and is only for information and general news purposes. It does not constitute an offer or invitation of any sort in any jurisdiction. Moreover, the information in this document will not affect Aura Group’s investment strategy for any funds in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Aura Group makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this information. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. You should not construe any such information or any material, as legal, tax, investment, financial, or other advice. This information is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The information may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This information is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in any way.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia.