When I was little, my dad would always pitch me business ideas. A personal favourite was riding a bicycle with a television attached. By all means a radical proposition in 2006, but something that is somewhat familiar in 2021.

Ideas are important but unfortunately, my dad is not the CEO of Peloton. There is a long painful road from idea conception to successful business. As the startup proverb goes,

“Ideas are cheap. Execution is everything.”

This article is written for my dad and I in 2006. More specifically, it’s written for founders who want to cross the chasm of ideation to execution. Just like the 6 year old me, there is still a lot I have to learn but I have tried to distil every resource I have read on the fundraising process to save you the time of doing the same.

Here is what the typical journey from idea to unicorn looks like.

I have an idea, show me the money…

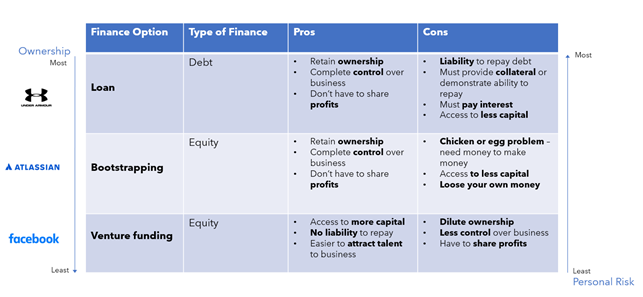

Ideas need money. At the onset, there are three basic options for financing a business:

P.s. Please skip to Stage 1 if this is too basic

Fundamentally it is a choice between debt and equity although they are not mutually exclusive. Equity is less risky but involves giving away part ownership of the business. Bootstrapping is a form of equity where the founder uses their own money and then reinvests profits to help the business grow. Venture funding is selling a percentage of ownership in your business to a venture capitalist in exchange for a sum of money.

Every billion-dollar company has a different financing story whether it be Under Amour’s founder maxing out credit cards or the Atlassian founders largely bootstrapping to global domination. Each has different pros and cons, the right choice of finance often lies in the magnitude of your idea. The more ambitious the idea, the more likely the founder will have to choose equity finance.

Bootstrapping a unicorn is every founder’s dream. These days in hyper-competitive global markets with record amounts of venture capital funding, it is very difficult to build a billion-dollar business without outside capital. While initial traction might be easier, competitors will be injected with cash to steal your customers.

“I think if you were going to do a start-up that was bootstrapped again today, you may really struggle to do that because these days the markets are connected more than ever before.”

What does the venture capital path look like?

Stage 1: Existential questioning

It sounds facetious, obvious and maybe even a bit stupid but I promise it’s not. Venture capital is not free money, it comes with strings attached. Not only are you giving up a degree of control and ownership in your business, but you are also signing an unspoken agreement to build the biggest company possible in the shortest period of time.

Occasionally this can lead to tension where the VC wants to swing for the fences and go after more markets while the founder wants to grow more conservatively.

Any potential conflict can be avoided by asking a simple question at the onset, do I really want to build a billion-dollar company? If after contemplation of the risk, stress and anxiety- the answer is still yes, proceed to Stage 2.

If the answer is no, they may conclude that venture funding might not be the right path. Venture capital is governed by power laws. Unlike a normal distribution, all the returns come from only a tiny fraction of investments. More than a decade of data reveals that out of more than 4,000 VC investment rounds annually, the top 100 generate between 70 and 100 percent of industry profits.

So venture capitalists are only looking for start-ups with the potential to be worth billions of dollars; any ambition less than that will dramatically reduce their odds of success. There is a lot of data behind the mathematics of venture if you want to read more.

Basically, venture capitalists live and die by finding that one unicorn.

It means the investor ethos is hyper-centered around outliers, many investor’s pupils expand as the rhetoric about, ‘category-defining, huge market, world first, total disruption and Uber for this…” increases. As a founder, being aware of the motivation of a VC is important and one that is often not talked about.

Great businesses are not always great venture-backed businesses.

P.s. Sometimes venture debt has proved a good option for businesses that don’t want to jump on the rocket ship of venture capital, check out Tractor Ventures.

Stage 2: Selling

The fundraising process is often called hitting the road. It’s usually a 6-month full time winding road populated with meetings, pitches and phone calls. The goal is for the founder to sell their idea to potential investors.

Before you meet with any venture capitalists, the path usually looks something like this:

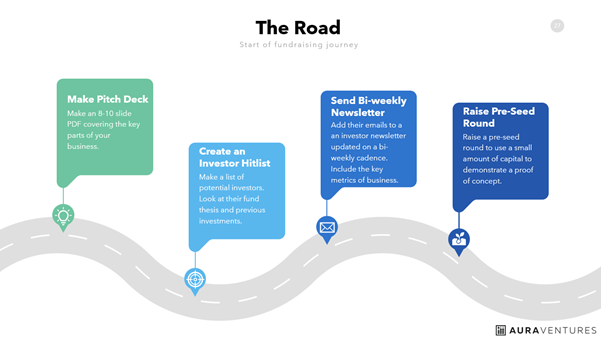

Bus stop 1: Preparing a pitch deck

The first thing founders do is prepare a ‘pitch deck’. It’s basically an 8–10 page slideshow that covers the most important parts of your business — the idea, the team, the market, potential traction and go-to-market strategies. It will generally be emailed to investors as a PDF. In practice, investors receive hundreds of these and will spend less than a minute skimming over each one.

A well-designed pitch deck that communicates the idea simply is often table stakes.

At Aura Ventures, the team has read 4,000 in the last four years. Here are some tips from the team:

Be very clear about what the business does or will do — don’t be afraid of being reductive, ‘a chatbot that responds to customer complaints’ is better than, ‘AI that disrupts the HR industry through IoT analytics’

The most important slides are the team, problem, solution and traction

Once the pitch deck is ready, it is time to make a hitlist! Rank angels, high net worth’s and VCs by their likelihood to invest in your company. Factors which are determinative are their investment thesis, prior investments and their personal career experience.

When making an investor hitlist, it’s important to include angels and high net worth individuals. These are usually the very first investors in your idea and have a much higher risk tolerance than institutional investors.

The easiest way to find them is to look for prominent companies in the industry you are entering and message the founders directly. For example, if you wanted to start a logistics-tech startup, look to see if Lindsay has a family office.

There are a lot of institutional investors and it can be a big waste of time meeting with ones who have no intention of ever investing in your company.

When assessing the likelihood, here are some things which you should look for:

Investment thesis: Do they only invest in certain industries? E.g. fintech

Investment stage: Do they only invest at certain stages? E.g. Series B (once you have lot’s of traction)

Investment lead: Do they lead investment rounds or do they only follow on? E.g. they only invest after others invest

Funds deployable: Do they have funds ready to deploy? (E.g. they might just be meeting with you for the relationship as opposed to actually investing)

ESVCLP requirements: Some VCs won’t actually be able to invest in your company if you operate a certain type of business such as lending or property development.

Founders may find it helpful to rank their hitlist by likelihood of investment and who they want to work with the most.

Bus stop 3: Send a bi-weekly newsletter

Once founders have a list, even before they are ready to raise funds, it’s really important to start developing relationships with investors before they go out to raise.

VC’s don’t invest in dots, they invest in lines.

This just means they can get a much better sense of you and your business over a long period of time (lines) as opposed to one or two zoom calls (dots).

The easiest way to solve this is by sending a bi-weekly or even monthly investor update to your hitlist. It could be as simple as this:The Good: 20% MoM growth, 2,000 new customer signs ups

The Bad: 5% churn (a one off this month because offboarding a big customer)

It is an excellent way to develop relationships with investors and allow them time to build up conviction in your company.

Stage 3: Raise a pre-seed round from Angels, family, friends or even the public

Industry jargon time; investors have special names for different stages of funding startups. In order, it goes pre-seed, seed, series A, series B…… Initial Public Offering

The stages are like checkpoints where you can only pass once your business has reached a certain level.

These levels are based off how much traction the business has had and how much money it needs before their next round of funding. If you are just starting your idea your first raise will likely be a pre-seed round. In Australia, this is typically financed by angel investors, friends, family or even the public (equity crowdfunding). Most people don’t have family and friends who can do this, which is why crowdfunding paltforms are so great for democratising capital for all.

Some companies skip this and go straight to seed.

A pre-seed round is all about taking a small amount of money (generally 100k-500k) to build out a proof of concept and get some traction. Traction can come in the form of sales interest, page views, product milestones or paying customers.

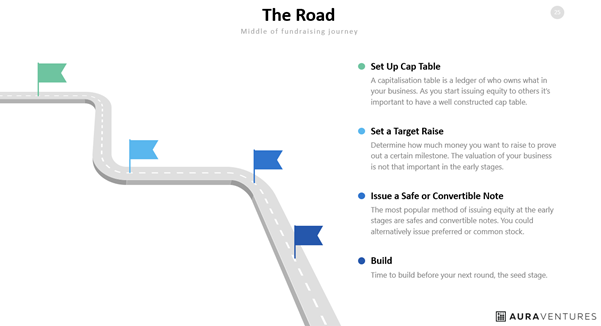

Bus stop 1: Set up a Cap Table

A well set out cap table is critical to getting investment. Many investors will turn down a business solely because of a poorly constructed cap table (if the founders don’t own enough of the business). It’s critical to set out a clear one and grasp key concepts like dilution, types of shares and debt/equity financing. Here are some great resources:

Before going out to angels and friends or family, founders will need to know money they need.

More specifically, how much money do they need to achieve a unit of progress to access more capital? That is the fundamental question for every business in deciding how much money to raise.

It is important for a business to project it’s cash runway and use of funds to have a clear sense of how much money it will need. They will need to have clear goals for how they will use that money, for a deep tech company it might be to get a certain approval, for a SaaS business it might be to have $10,000 in monthly reoccurring revenue.

Achieving this unit of progress will unlock more money in later rounds.

Bust stop 3: Issue a SAFE or convertible note

For most founders, the next step is to issue equity to their early stage investors. Most commonly, founders will use a SAFE note or a convertible note. These instruments start as a debt then convert to equity at the priced round. In investor land, a priced round is when your company is given a valuation by investors. At the pre-seed stage, this can be awkward and difficult to do for angels and family or friends. Basically, it defers all the technical nitty and gritty stuff for the institutional investors.

After building, founders will then start pitching the VCs on your hitlist. Generally, they should already know the business from their newsletter If they don’t, they will try and get a warm intro from a mutual connection. If they don’t have any, that’s also fine, they can apply for investment on the website or message an investor directly.

From my experience, this is usually how the process goes:

1. Send investors a PDF of your pitch deck

2. Meet with a junior analyst or associate for a 30 minute zoom meeting

3. Meet with a senior principal or partner in person or for a longer zoom meeting

4. Answer a lot of questions over email + send more information

5. More meetings and more emails

6. They want to invest

The whole process is like a funnel and fewer and fewer companies progress to the next stage. Most VCs will say no 100x more than they say yes. End to end, the process lasts about 7–8 weeks from first meeting to final investment. Now multiply this by the number of investors you are pitching and it quickly becomes a full time job with about 40 meetings a week.

Here are some tips from the team to make the process easier:

Automate as much as possible: The best founders use Calendly to schedule meetings and Loom to record them doing their pitch deck. It is probably the biggest hack to record your 30 minute pitch and then send it out to investors alongside your pitch deck. This speeds up the process significantly.

Don’t spend time with investors who don’t seem that interested, double down on the ones that do

Don’t get disheartened. Investors are wrong more than they are right — it’s often like a teacher who has never taught history marking a history essay based only off a marking rubric

Jargon tip: Raising 1 million for 25% in the company, means a pre-money valuation of 3 million and a post-money valuation of 4 million

Stage 5: Hit milestones and become unicorn

If founders get seed investment from a VC, the rest of the road is about hitting pre-determined milestones and unlocking more funding. Typically each of these milestones occurs after 18 months, where the VC decides whether to keep investing.

The company’s valuation should be increasing at each funding round otherwise they will probably not keep investing.

These funding rounds span from a seed round all the way up to Series A,B,C,D,E.

It’s a long road from idea to unicorn, but help explain the journey and the stops along the way.

This article was written by Sean Stuart, Investment Analyst at Aura Ventures, and originally appeared on Medium. For more from Sean, you can follow him here.