VENTURE CAPITAL

Gravity and Growth in the Australian Venture Capital Market

The talk of never-ending growth can be worrying in investor land, as everyone knows — what goes up must come down.

Global markets are reeling from the US-Israel-Iran war, with surging energy prices, weakening currencies, and growing recession fears dominating the outlook.

This outlook contains information correct as at 1400hr on 07 Apr 2026

As the US and Israel's war against Iran enters its sixth week, the impact on global economies are being felt. The prolonged closure of the Straits of Hormuz, through which about 20% of seaborne oil and significant trade pass, has led to high energy prices and supply chain disruptions. Historically, a 50% or more rise in oil prices has almost always been followed by a recession.

The US, on the other hand, should be more insulated from high energy prices, as a net exporter, even though gasoline prices in the US are up by USD1.00 per gallon. It could insulate its own economy further with an energy export ban.

The latest employment figures from the Bureau of Labour Statistics, released on 3 Apr, showed March Non-farm Payrolls at +178,000 (well above the Bloomberg estimate of +65,000), the largest increase since Dec 2024 (+237,000). The Unemployment Rate unexpectedly eased lower to 4.3% (from 4.4% in Feb). This might cause the Federal Reserve to pause further interest rate cuts in early 2026. Two rate cuts are expected in June and Q3, taking FFTR to 3.25% from the current 3.75%. However, persistently high energy prices may delay cuts, as they curb hiring and weaken labour.

Taking a cautionary stance, Federal Reserve chair Jerome Powell said, “We don’t know what the economic effects will be. The tendency is to look through any kind of supply shock, but a critical essential aspect of that is you have to carefully monitor inflation expectations.” On the turmoil in the Private-credit markets, “we’re watching it super carefully. I’m reluctant to say anything that suggests that we’re dismissive of the risk, but we’re looking for connections to the banking system and things that might, you know, result in contagion.”

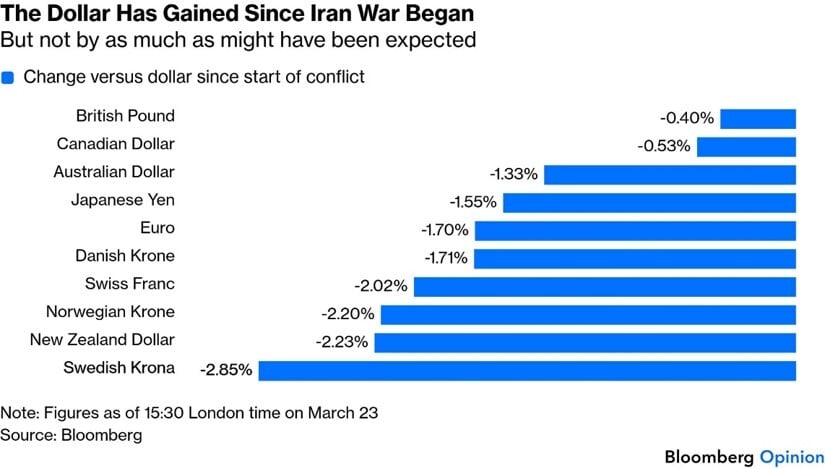

Foreign exchange markets have also been impacted by the war in the Middle East. The USD is the leading safe-haven currency in times of crisis. It has appreciated across the board against the G10 currencies, even against the Swiss Franc and the Japanese Yen, which are normally regarded as safe havens. Currency volatility matters for investors because it can quickly reduce the real value of financial assets held in depreciating currencies.

There are no reliable safe havens for investors seeking refuge from Black Swan events like the Iran war. After the war started, Gold plunged 26.7% below its January historic high of USD5,595 to USD4,099; it has since recovered some ground to around USD4,600. Bitcoin plunged from around USD126,000 in October last year to a low of USD60,000, before trading around USD69,000 at the time of writing.

Even if the Straits of Hormuz were to reopen, it would take months, perhaps even one to two years, for Oil and Gas prices to return to pre-war levels, as much damage has been done to production facilities.

Overnight, US 10-Year Treasuries closed up 0.01% at 4.34% (3 Mar 4.04%), Australian 10-Year Govt Bonds closed down 0.05% at 4.99% (3 Mar 4.75%), and Euro 10-Year Bonds closed up 0.01% at 2.99% (3 Mar 2.71%).

Sources: Bloomberg, MSNBC, Reuters, Morningstar, Business Times, 07 Apr 2026

As an exporter of crude oil, natural gas (the world’s 2nd largest LNG exporter) and coal (also the 2nd largest), the Government has reduced the petrol and diesel tax for three months to cushion the impact on consumers. RBA raised the OCR by 0.25% to 4.10% on 17 March, citing inflation risks from the Iran-related energy shock and a resilient labour market. However, despite a positive interest rate differential against the USD, AUDUSD has not benefited, as it remains under pressure.

AUDUSD is challenging the lower end of the 0.6900-0.7000 Support area. In the coming weeks, we can expect AUDUSD to drop to the 50% Fibonacci Support at 0.6750.

EURUSD

The Eurozone is feeling the economic pain of the Iran war. Eurozone inflation in March increased by the most since 2022, when Russia launched a full-scale invasion of Ukraine. Countries in the bloc are slashing their economic outlooks and hoping to avoid a recession. The outlook for EURUSD looks negative.

As expected, EURUSD in March headed toward and even broke through the 50% Fibonacci Support/Resistance area at 1.1490. EURUSD is now trying to consolidate above this support, but the technical picture suggests another potential decline towards the 1.1150-1.1200 area.

Image Source: Bloomberg 07 Apr 2026

GBPUSD

GBPUSD is under pressure even though the BoE held its Bank Rate steady at 3.75% on 19 Mar and signalled a sharply more hawkish view. GBP still suffers from the UK’s myriad of political, social and economic problems.

GBPUSD’s continuous drop after failing to hold above 1.3650 has broken into the 1.3200-1.3400 Support Zone, with consolidation in March. GBPUSD is now testing the lower 1.3200 Support. This might give way in the next few weeks, heading for the next Support at 1.3000.

Image Source: Bloomberg 07 Apr 2026

USDJPY

The JPY continues to weaken, with USDJPY testing the psychologically important 160.00 level.

Japanese Finance Minister Katayama has hinted at intervention as the authorities are growing concerned that currency markets are turning increasingly volatile. Intervention will have a limited effect due to the current geopolitical situation. Markets expect the BoJ to hike rates by 0.25% as early as this month, which could be more supportive of JPY.

USDJPY faces strong resistance at the 160.00 psychological level. Technically, there is a strong likelihood of a break with USDJPY moving up along the Uptrend Channel to 162.50.

Image Source: Bloomberg 07 Apr 2026

USDSGD

The Monetary Authority of Singapore (MAS) is likely to tighten monetary policy at its next MPC meeting on 14 April, potentially strengthening the SGD. Unlike other Central Banks, the MAS uses the SGD to manage monetary policy and control imported inflation. With crude oil prices expected to remain around USD80–USD100 per barrel for an extended period, inflation for 2026 is forecast to range from 1% to 2%, up from the previous forecast of 0.5% to 1.5%.

Having broken above Resistance at 1.2800, USDSGD is consolidating below 1.2900. After this, we can expect USDSGD to move back below 1.2800 and consolidate between 1.2600 and 1.2800.

Image Source: Bloomberg 07 Apr 2026

AUDSGD

After failing to take out Resistance at 0.9100, AUDSGD suffered a prolonged drop in March towards Support at 0.8800 as we expected. We could see a period of consolidation between 0.8800 and 0.8930 before a challenge to break below towards 0.8600.

Image Source: Bloomberg 07 Apr 2026

XAUUSD

Gold fell as much as 22% at its lowest (USD4,099) after the US/Israel–Iran war started, before recovering to around USD4,650–USD4,700. The sharp fall has been attributed to

the need for investors to liquidate their positions and cover losses elsewhere. Technically, we are likely to have seen Gold’s top for some time. If the USD4,500 level does not hold and Gold remains below the 50-Day Moving Average over the next month or so, the market might start to explore downside in XAUUSD.

Image Source: Bloomberg 07 Apr 2026

Note: In the Candlesticks Chart, Green bars mean the Close is higher than the Open price, and Brown bars mean the Close is lower than the Open price

The talk of never-ending growth can be worrying in investor land, as everyone knows — what goes up must come down.

We're excited to announce the signing of a share purchase agreement by Aura Ventures for its investment in Integrated Portfolio Solutions. The...

We are thrilled to announce the appointment of Dan Annan as our new Distribution Director. With a career spanning over two decades in the financial...