As we endure volatile market conditions, many investors are rightfully looking into their portfolios and examining their asset allocations.

As an exercise in this, let’s examine my family’s portfolio and understand my objectives, strategy, risk considerations, and a peek into the future.

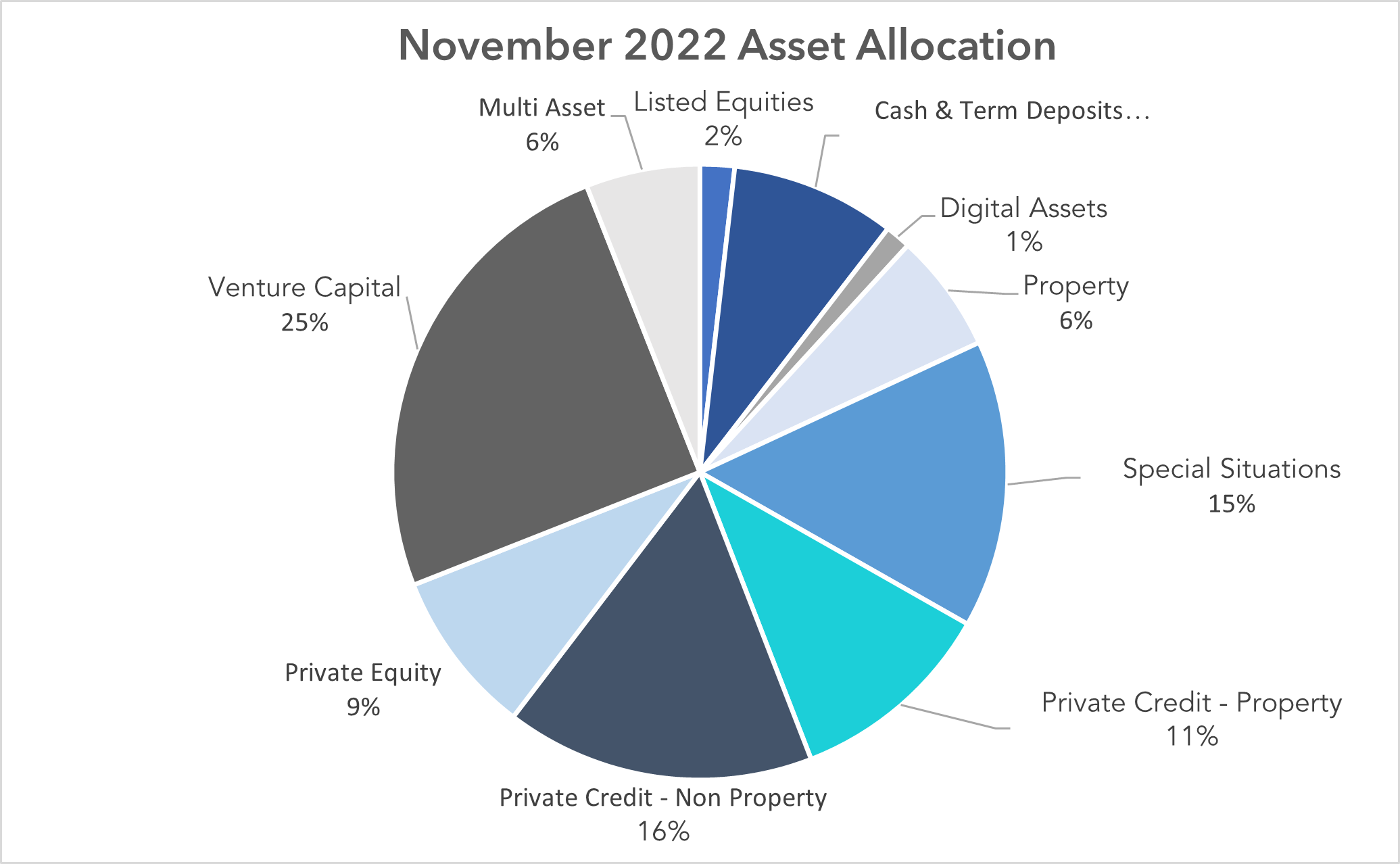

The Breakdown

As of November 2022, my family’s asset allocation is as follows:

As this is a high-level summary, please note that it may suffer from minor data entry issues. It also excludes direct property interests, shares in an Australian bank where I am a non-exec director, Aura Group shares and collectibles such as my personal watch collection.

And, as you might have guessed, a significant amount of the asset allocations listed above are via Aura Group managed funds, including venture capital, private equity, special situations, private credit, multi-asset, property, and cash & term deposits. I am a fee-paying client of Aura Group, and I do not get special fee discounts or rates.

Investment Objectives and Strategy

When looking into my family’s portfolio, my main objective is to achieve a return after fees at least equal to CPI inflation +6% per annum over a rolling 7-year period. Given long-term inflation targets of 2-3%, this equates to a medium to long-term target of at least 8-9% per annum. I have not calculated the actual net returns over a time series, as this portfolio occurs across various entities and structures. I believe that this has been achieved given the net returns of most of the funds in the portfolio over the last five years.

Asset Allocation Considerations

Several factors have contributed to the choices I have made for my family’s asset allocation.

Personal Characteristics

Due to my age, my salaried income, and my profession, I am more comfortable accepting a higher risk profile than other people may be. Being relatively young, I have 25-30 high-earning years until I retire, meaning I have time on my side to ride out potential volatility than if I had, say, 10 working years left. Because I invest for a living, I feel comfortable taking higher risks than someone who may not be a sophisticated investor.

Liquidity of Investments

When I was younger, my portfolio was definitely more concentrated. I had an allocation bias to more illiquid asset classes, such as venture capital and private equity. However, as I have gotten older, I have pivoted to more liquid alternatives, like shorter duration private credit, multi-strategy, and special situations.

Benefits of Diversification of Investments

Despite my high-risk investment profile, I still decided long ago that it was paramount to have a well-diversified investment portfolio.

To assist with our transition to a single-income family—and the extra costs that have come since welcoming my twin girls—the need for income has increased. Therefore, about half of my portfolio is invested with the aim of generating regular income, with a further 8% in cash and term deposits that after recent interest rate hikes also deliver nearly 3% per annum with access to liquidity.

Miscellaneous notes

When looking at the breakdown of my asset allocation, it is important to note that venture capital appears disproportionate due to over five years of capital growth for earlier vintages. While I am a strong believer in the potential of blockchain technology in real-world use cases, the exposure is predominantly via picks and shovels venture capital, rather than to cryptocurrencies themselves.

Looking forward

In our current market conditions, bonds and equities may become more attractive. I hope our tactical opportunities and multi-asset strategies will provide greater portfolio exposure to both. Based on current expectations, I am looking to increase my exposure to private equity via my family’s portfolio.

Important information

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Group and related entities and is only for information and general news purposes. It does not constitute an offer or invitation of any sort in any jurisdiction. Moreover, the information in this document will not affect Aura Group’s investment strategy for any funds in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Aura Group makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this information. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. You should not construe any such information or any material, as legal, tax, investment, financial, or other advice. This information is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The information may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This information is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in any way.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia.

Family offices sit at the intersection of wealth and legacy. But without a clear framework, even the most successful families can struggle to manage...