PRIVATE CREDIT

Aura Private Credit Weekly Insights - 27 January

With the persistent inflationary pressure not yet showing any signs of slowing, further RBA rate rises are certainly on the cards.

This week, the RBA’s has identified additional considerations that will influence future rate decisions, with a hint of a slowdown in rate rises.

This week's insights are focused on the RBA’s minutes released earlier in the week. The RBA has identified additional considerations being made that will influence their future rate decisions, with a hint of a slow down in rate rises.

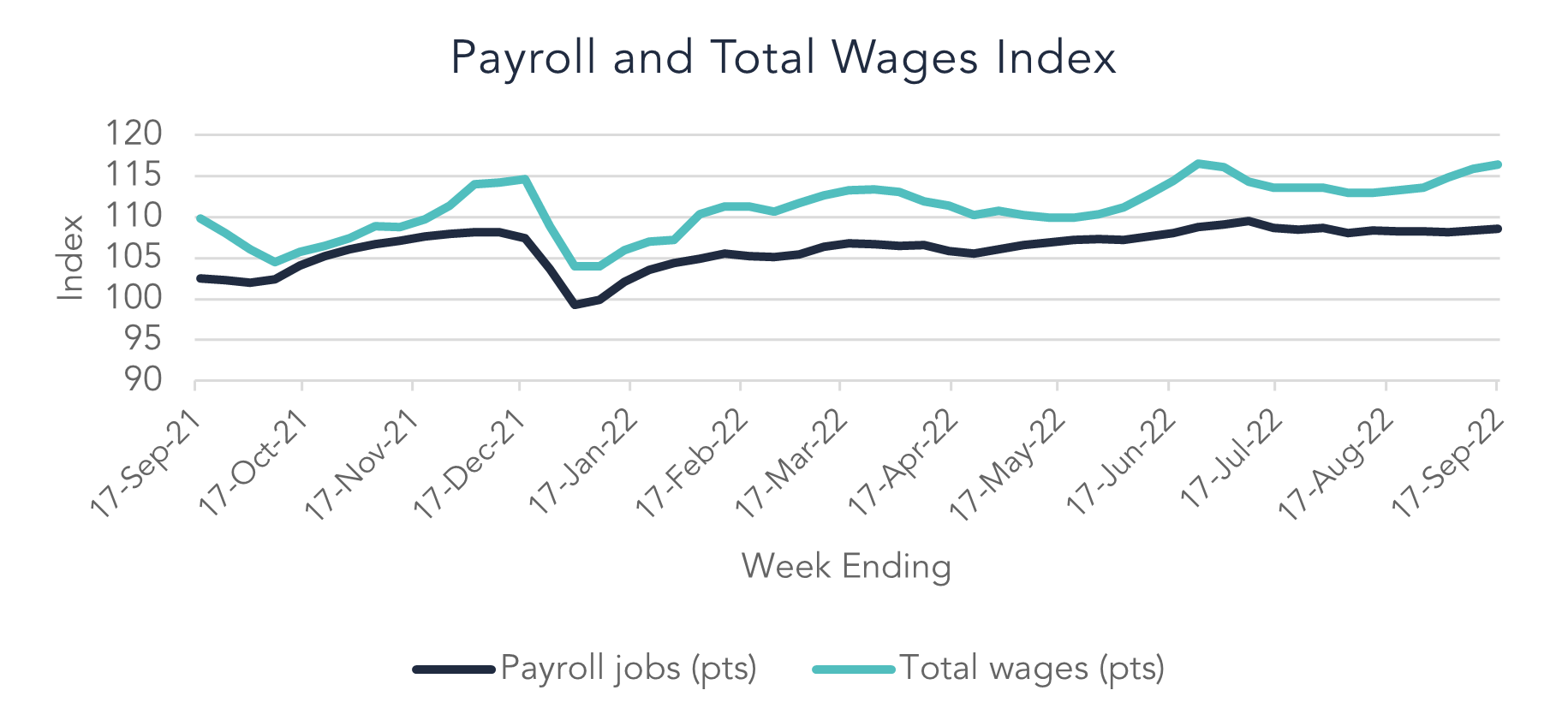

Data from the latest payroll, jobs and wage estimates recorded is for the two weeks up until the 17th of September shows that:

Payroll jobs were up 0.4%, compared to a decrease of 0.1% in the previous fortnight, and

Total wages were up 1.4%, compared to an increase of 1.3% in the previous fortnight.

As a result of the extremely tight labour market, payroll jobs have demonstrated slow growth over 2022. The average monthly growth over the past six months has been 0.3%. This time last year we were facing very different labour market conditions due to the Delta Covid-19 variant, where payroll jobs fell due to lockdowns.

The rise this month was experienced across all states and territories with the ACT and WA leading the rise, up 0.7% and 0.6% respectively. The education and training industry accounted for more than a third of the payroll job increases. Wages paid over the month to mid-September were up 2.7%, largely driven by the payment of periodic bonuses across multiple industries which tends to occur around September every year.

Ongoing wage pressure is expected to continue as inflation remains and the cost of living continues to rise.

After two years of little increase, overseas migration has begun to significantly contribute to Australia’s recent population growth. The country has experienced a large increase in yearly arrivals, which is up 183% as of March 2022. With additional skilled migrants being able to return to Australian shores due to reduced restrictions, we would expect to see the labour market begin to adjust accordingly.

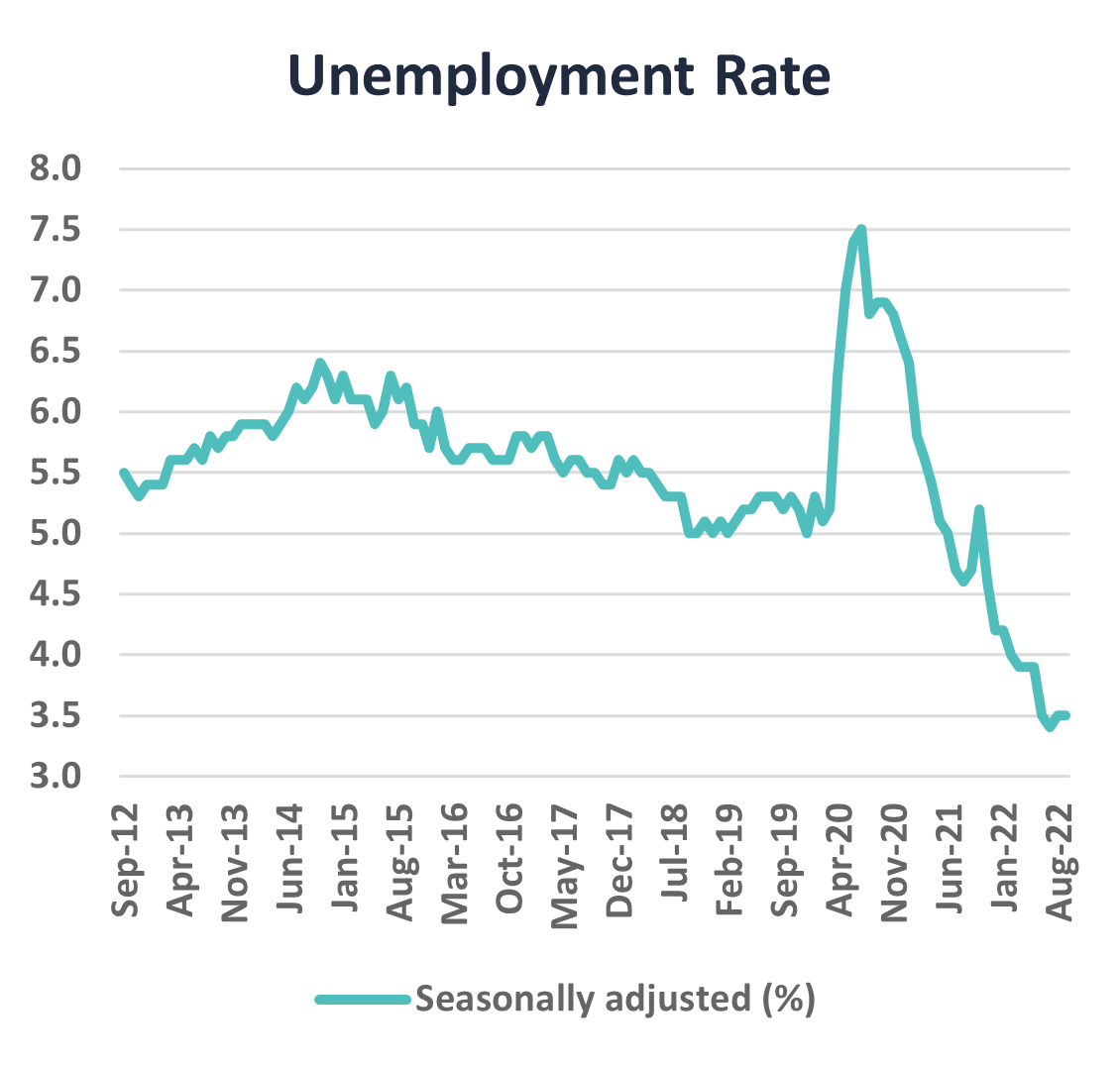

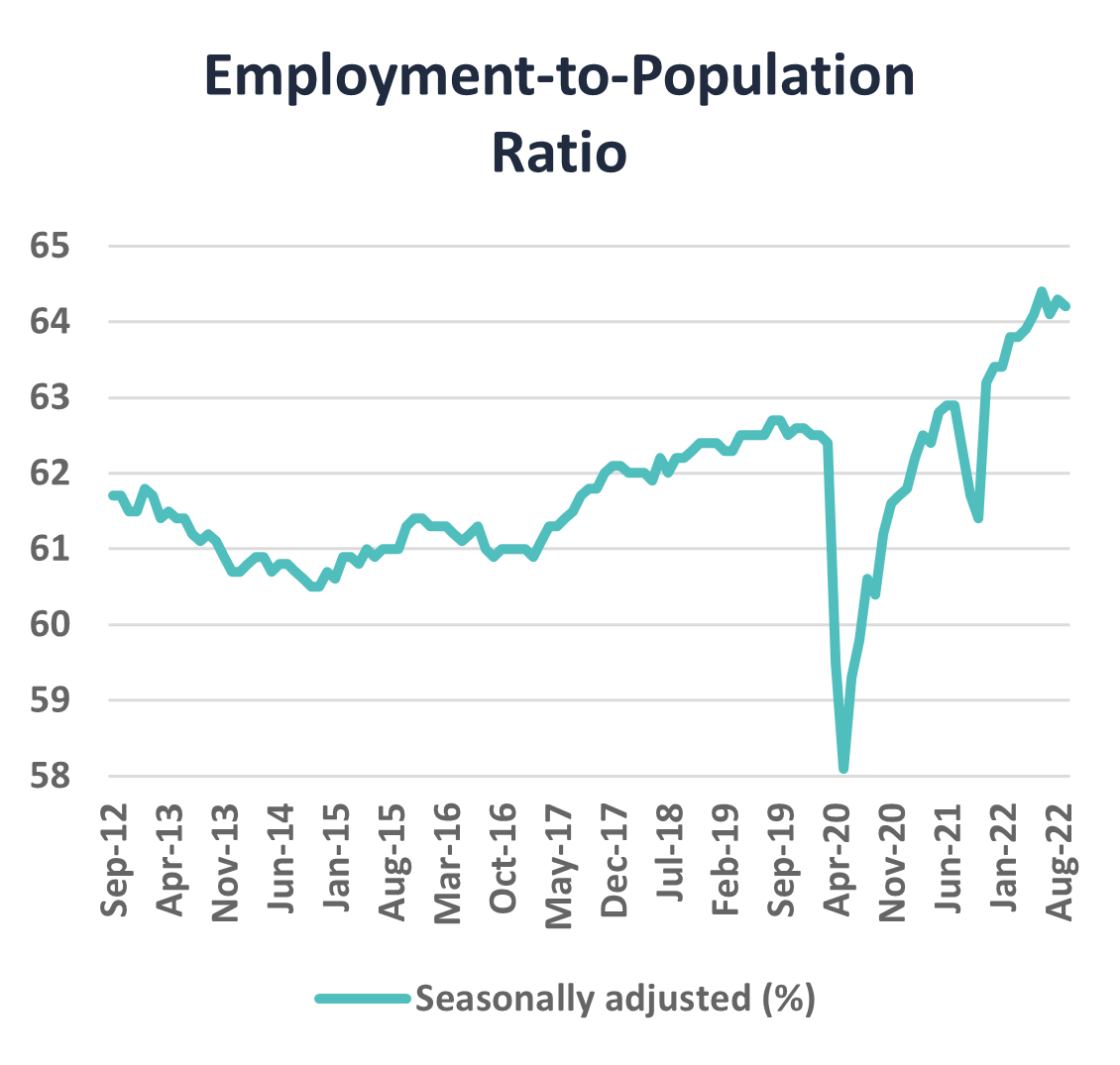

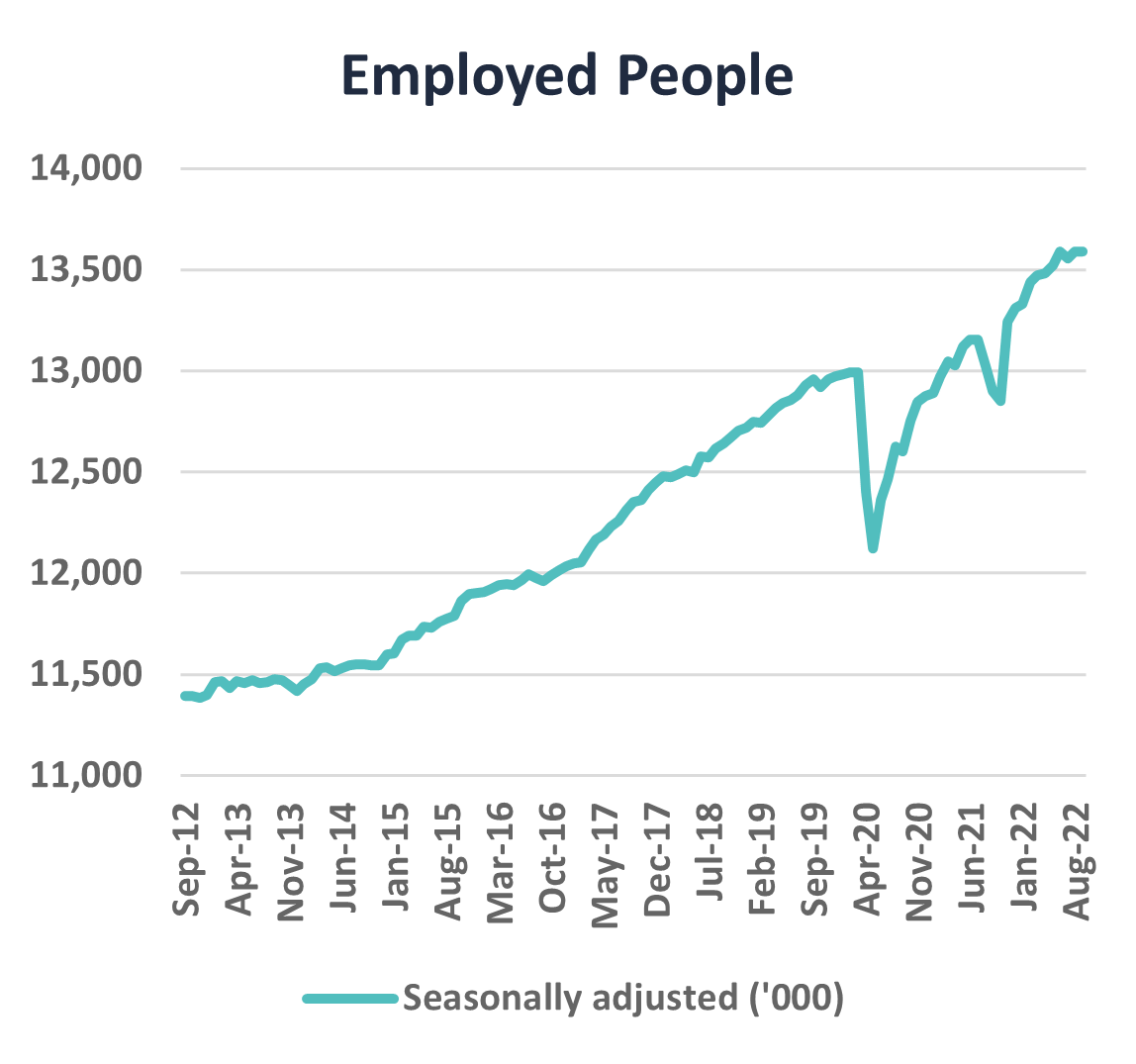

The September Labour Force statistics were released on Thursday, 20th of October, displaying early signs of stabilisation across most indicators:

The unemployment rate remained unchanged at 3.5%, 1.7 percentage points tighter than the March 2020 spike at the commencement of the COVID-19 pandemic;

The number of employed people increased slightly, by 900 people. However, on a trend basis, has displayed a clear deceleration of its recent month on month increases;

The employment to population ratio dipped ever so slightly by 0.1%. However, in trend terms, has remained stagnant for the past three monthly reads;

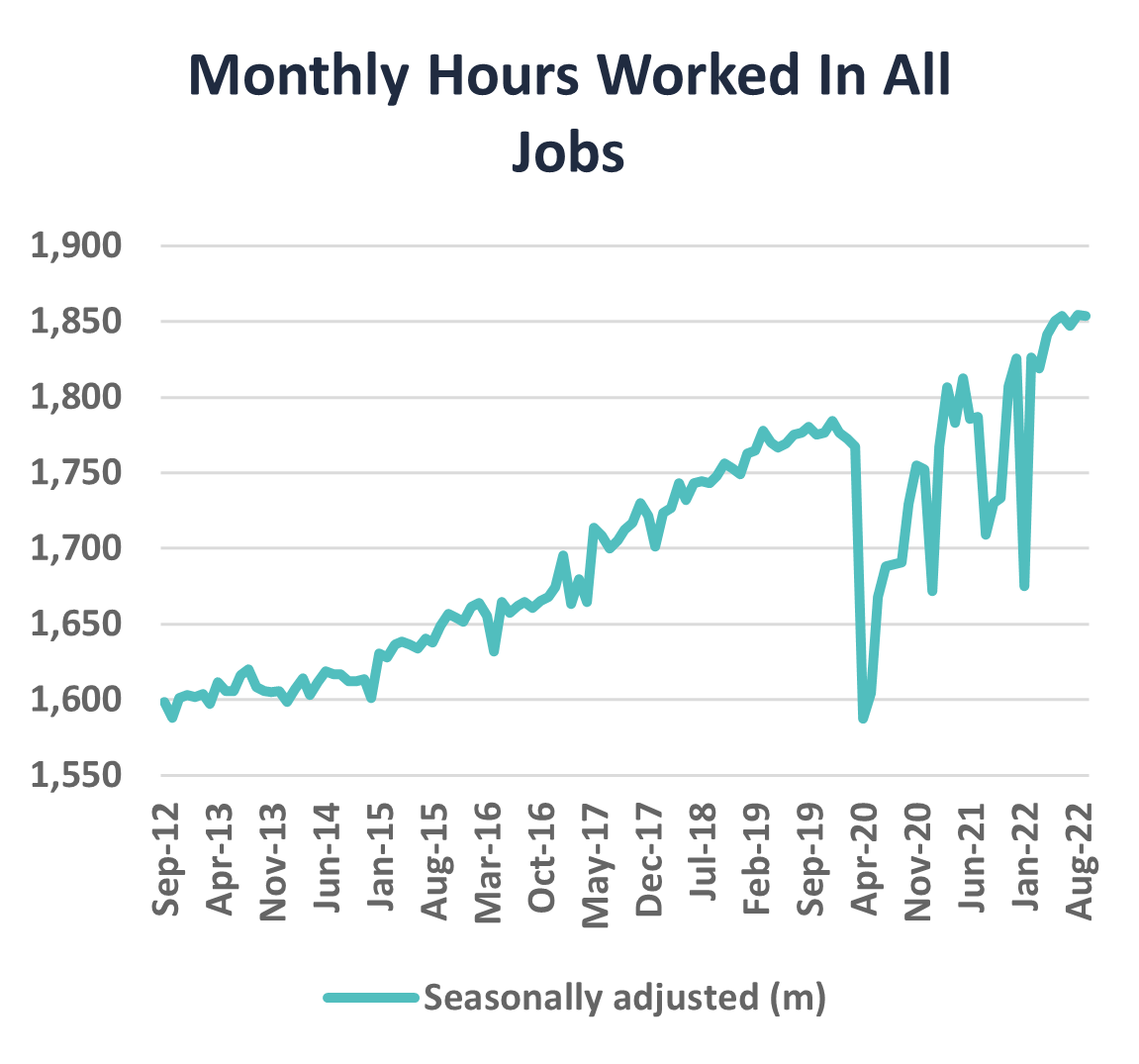

Monthly hours worked across all jobs saw a micro contraction and has hovered around the same level for the past five monthly reads.

It is the investment team’s view that the tightness of labour market is at or near peak, operating in excess of its sustainable potential. We anticipate a mean reversion will be experienced over the coming data releases. This reversion will likely be driven by the return of migration and increased cost of capital as a result of the lagging impact of the RBA’s interest rate hikes and quantitative tightening, that will likely lead to the dampening of both consumption and investment.

Michele Bullock, Deputy Governor of the RBA, delivered a speech on Tuesday 18th October that provided insight into the RBA’s decision to increase the cash rate by 25 basis points as opposed to another widely anticipated 50 basis points, in line with the movements of most other central banks across the developed world.

The Deputy Governor stated that it was clear across all board members that a further rate increase was necessary. Inflation was too high and is anticipated to increase further, fuelled to some extent by demand-side factors. Additionally, unemployment is at its lowest level in around half a century, which is expected to translate into upward wage pressure, further fuelling domestic inflationary pressure.

It was accepted across the board that interest rates have some way to go in order to achieve the target inflation rate of 2–3 per cent. However, discussions have turned to the appropriate size of increases moving forward, particularly given the RBA’s ability to reset its cash rate monthly (with the exception of January), which is broadly more frequent than many central banks, such as the Federal Reserve or the Reserve Bank of New Zealand. It was the investment team's interpretation that the RBA Board will continue to increase the Cash Rate over the remaining two meetings of the year at 25 basis points per meeting – in line with current market pricing. We will pay close attention to household consumption data, particularly over the January break, before reassessing monetary framework over 2023, with decisions commencing February 7th.

Sources:

1 Source: Australian Bureau of Statistics – Weekly Payroll Jobs and Wages in Australia, September 2022

2 Source: Australian Bureau of Statistics – Return of Overseas Migration Spurs Australia’s Population Growth, September 2022

3 Source: ABS – Labour Force, Australia, September 2022

4 Source: Reserve Bank of Australia – Speech; Policymaking at the Reserve Bank

With the persistent inflationary pressure not yet showing any signs of slowing, further RBA rate rises are certainly on the cards.

Exploring the RBA cash rate, inflation and underlying components in this week's Aura Private Credit Weekly Insights.