Monthly CPI

.png)

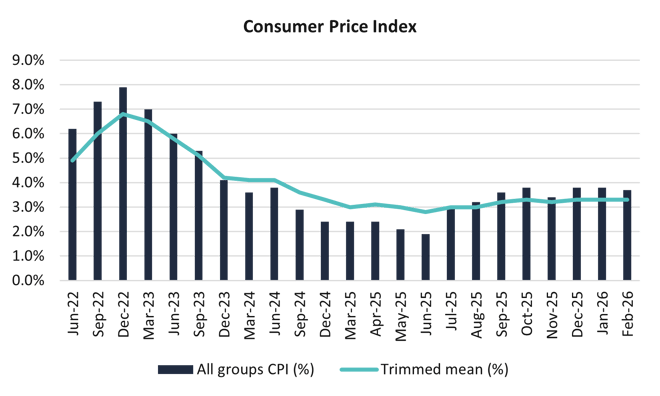

The February 2026 monthly CPI indicator shows that inflation remained persistently elevated ahead of the Middle East conflict, with only marginal signs of easing. Headline CPI rose 3.7% year-on-year, down slightly from 3.8% in January, while underlying inflation held at 3.3%, remaining above the RBA’s 2–3% target band. This indicates that disinflation had stalled in the steady-state environment, with inflation stabilising above target rather than continuing a clear downward trend. Against this backdrop, the emergence of a significant energy supply shock has materially shifted the outlook, prompting economists to debate how many additional rate hikes the RBA may deliver over the remainder of the year.

Domestically, inflation pressures remain broad-based, led by housing, which increased 7.2% annually. This reflects continued strength in rents, new dwellings and electricity, with the latter rising sharply due to the expiry of government rebates. Food prices rose 3.1% and recreation and culture 4.1%, pointing to persistent services and discretionary inflation. Transport provided a partial offset due to earlier declines in fuel prices, though these moves predate the recent surge in global oil prices.

Crucially, the February data does not yet reflect the inflationary impact of the Middle East conflict, which has pushed oil prices materially higher and is expected to lift headline inflation in the coming months. Jim Chalmers has warned inflation could rise toward 5%, while economists argue the shock will add to already strong domestic momentum. With the economy entering this period from a position of resilience, characterised by solid income growth, tight labour markets and strong investment, the oil shock is likely to act as “fuel on the fire” rather than the primary driver of inflation.

For the RBA, persistent core inflation and strong domestic demand suggest policy must remain restrictive, while the external energy shock adds further upside risk. Economists are forecasting anywhere between two and four additional rate hikes, equating to a cash rate of 4.6%-5.1%, as the RBA seeks to contain inflation expectations. At the same time, there is a growing risk that the combined effect of higher rates and elevated energy costs will slow the economy, potentially leading to weak growth and increasing the risk of a recession over the medium term.

Source: Australian Bureau of Statistics, Consumer Price Index, Australia, March 2026.