PRIVATE WEALTH

Monthly Forex Outlook - October 2025

Global risk sentiment held steady as financial markets chose to ignore the third US Government shutdown under President Trump’s watch.

RBA Assistant Governor Christopher Kent outlines the lags in monetary policy, giving insight into likely softening in demand-driven inflation.

The RBA’s two key levers with respect to fighting inflation include Quantitative Tightening and hiking of the official cash rate. A recent speech delivered by RBA Assistant Governor Christopher Kent outlines the lags in these forms of monetary policy, giving insight into likely softening in demand-driven inflation.

We figured we would take this opportunity to go over why these forms of monetary policies lag, and what may happen in the short to medium term.

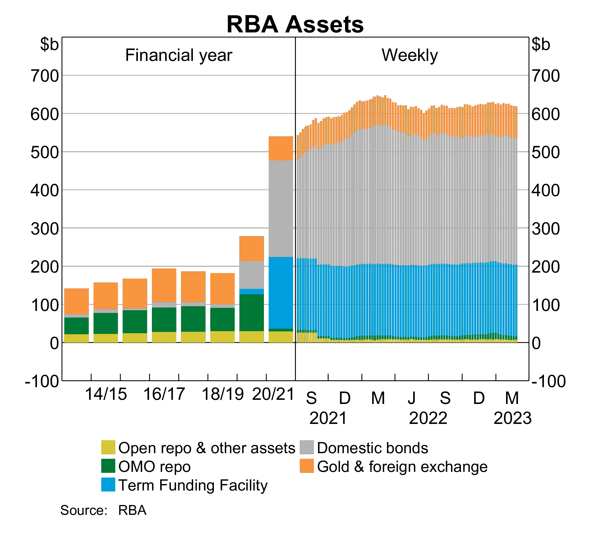

Over the course of the pandemic, particularly in 2020 and 2021, the Reserve Bank of Australia implemented quantitative easing as a means of expansionary monetary policy. This unprecedented policy action involved the creation of money that was subsequently lent to:

Australian Banks (ADIs) via the Term Funding Facility (TFF);

State Governments via Semi Government Bonds (Semis); and

The Federal Government via Australian Government Securities (AGS).

This increased the money supply within the economy with the intention of elevating economic activity.

Unfortunately, the expansion in money supply, relative to goods and services, is a contributing factor behind the elevated level of inflation Australians are currently experiencing.

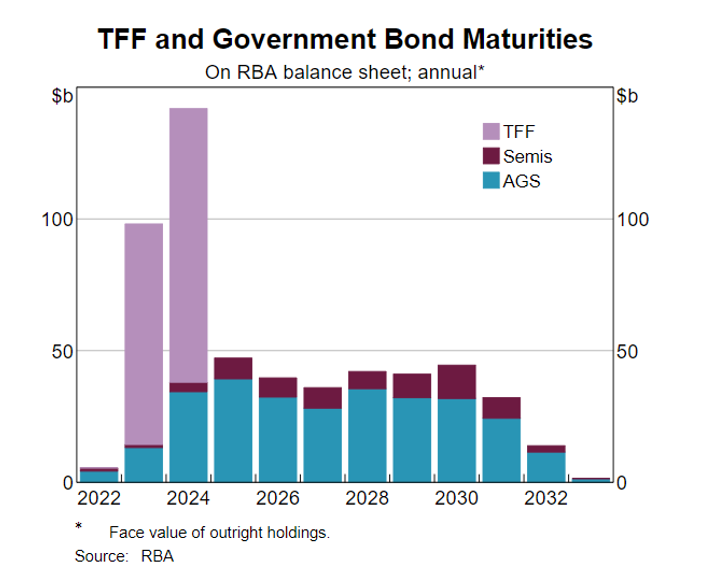

Graph C

To counter the inflationary pressure created via quantitative easing, the Reserve Bank of Australia has chosen to enact quantitative tightening, whereby it is reducing the money supply. As outlined by Assistant Governor Christopher Kent the deflationary effects of quantitative tightening lag relative to the expansionary effects of quantitative easing.

This will see scheduled quantitative tightening take effect meaningfully over 2023 and 2024, due to the repayment of the TFF, although not entirely until 2033. Unfortunately, the lag effect of quantitative tightening means it is not an effective tool to bring inflation back to the target range over the short to medium run. The demand must reduce through another mechanism.

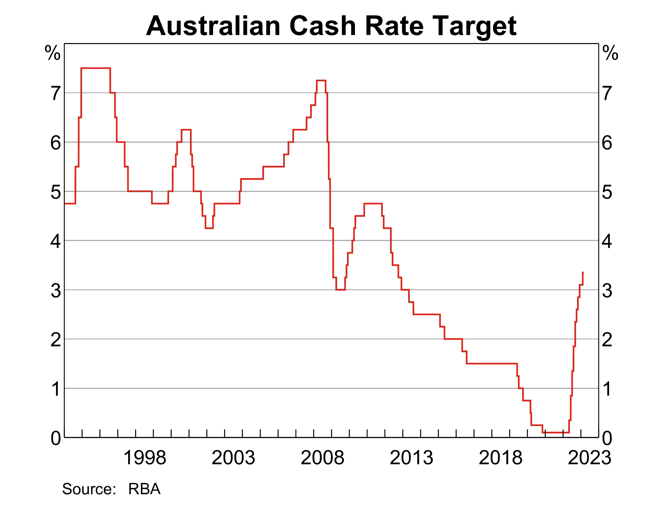

To reduce the money supply, the RBA will wait for ADI’s, state governments and the federal government to repay the TFF money, Semi’s and AGS’ extended during the pandemic and destroy the repaid funds, reducing the supply of money within the economy. There is a lag because these debt instruments follow varied repayment profiles, displayed in Graph B. Traditional contractionary monetary policy, that is increases to the official cash rate, is a more efficient and flexible tool than the scheduled quantitative tightening. However, is still somewhat blunt and lagged.

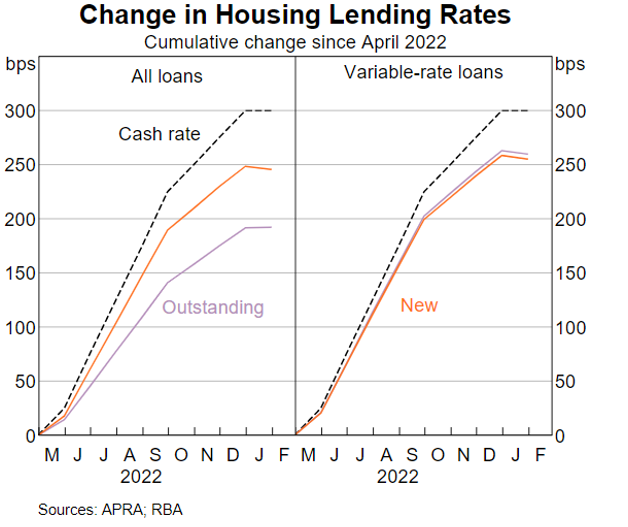

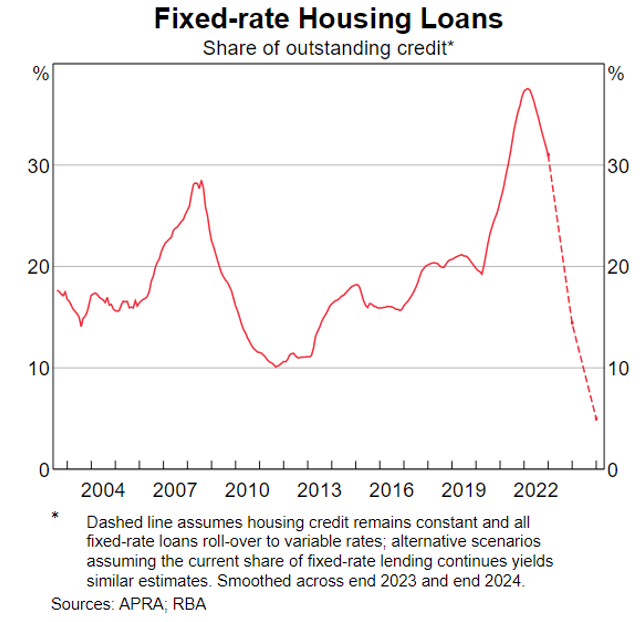

The first change within the economy contributing to a lagged effect of traditional monetary policy is the abnormally high share of fixed-rate mortgages, seen in Graph D. Fixed-rate loans peaked slightly above 35% of all housing credit and remains elevated above the 30% mark. Household borrowers of these loans have experienced no impact from the 3.50% increase to the RBA Cash Rate with respect to their mortgage repayments. In other words, their disposable income, which drives aggregate demand, has not been stripped away by elevated interest repayments (a primary objective of traditional monetary policy).

Recent monetary policy actions will have a lagged effect on these borrowers as they roll off of fixed-rate mortgages and the share of borrowers on variable loans increases – expanding the effectiveness of traditional monetary policy.

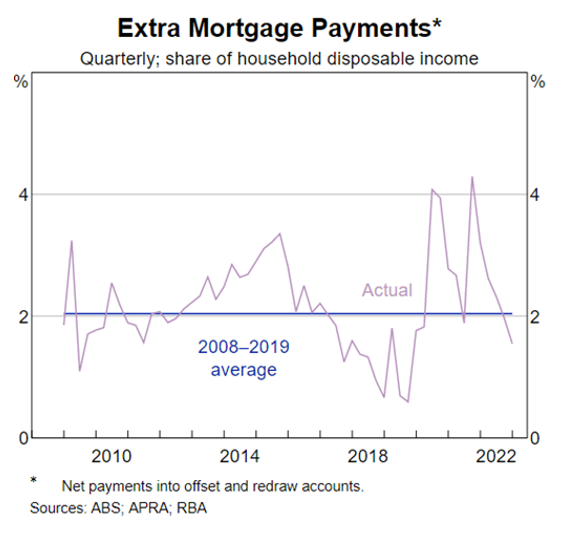

The second contributor to a lagged effect of traditional Monetary Policy includes savings buffers built up by households over the pandemic. Throughout the pandemic the average household income increased due to stimulus measures and, as we all recall, consumption options were significantly curbed. This led to record levels in the rate of household savings and extra mortgage payments.

Accumulated savings can be drawn down by borrowers, should they choose, to sustain their spending in the face of rising interest rates and cost-of-living pressures. To give a sense of the size of the additional mortgage buffer (ignoring other forms of savings), the RBA states that if borrowers decided not to make any extra mortgage payments for a time, it would take around one year for the buffer built up during the pandemic to run down.

Indebted households’ willingness to draw on these and other savings buffers will dictate the degree to which the intended effect of monetary policy is lagged and the degree to which the Cash Rate is increased.

Despite a promising monthly read in the January monthly CPI indication, we have not seen a decline in the official quarterly CPI read. The RBA’s primary objective is to maintain inflation between 2-3% and it will do what is necessary to achieve that goal.

The investment team is beginning to see investor returns benefiting from increases to base rates, while keeping a close eye on the portfolios to ensure serviceability stresses for underlying SME borrowers are managed early.

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887). Aura Funds Management Pty Ltd is the Trustee of all the Funds mentioned and a subsidiary of Aura Group Pty Ltd.

Any financial product advice given in this report is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs. Aura does not guarantee the performance of its funds, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report is based on the information provided to Aura by third parties that may not have been verified. Aura believes that the information is reliable but does not guarantee its accuracy or completeness. Aura is not able to give tax advice and accordingly, investors should obtain independent advice from an accountant and/or lawyer before making any decision based on the tax treatment of its investors. You must read the Fund Fact Sheet or Information Memorandum and seek professional advice before making a decision to invest in any of the funds.

Global risk sentiment held steady as financial markets chose to ignore the third US Government shutdown under President Trump’s watch.

Australia's Gross Domestic Product grew by a modest 0.2% in the March 2025 quarter, a down from the 0.6% growth recorded in the December 2024 qtr.

While most investors expect prices to increase as the global economy recovers, concerns about the speed and trajectory of the recent rises persist