Have you ever heard of the proverb “shirtsleeves to shirtsleeves in three generations”?

For family wealth, the saying refers to the historical propensity of ~70 per cent of enterprises to fail by the time the founder’s grandchildren take a leadership role.

In the book Preparing Heirs: Five Steps to a Successful Transition of Family Wealth and Values, Victor Preisser and Roy Williams noted that research they had conducted indicated that the major causes of financial collapse in family wealth transition have more to do with trust and governance in the family than with legal, financial, or business planning. By percentage, the main causes they found were:

Loss of wealth due to a collapse in trust and communication in the family system (42%)

Loss of wealth due to heirs being inadequately prepared for creating and managing wealth (17%)

Loss of wealth for lack of proper governance structure (8%)

Loss of wealth for insufficient tax and legal planning (3%)

Successful wealth transition over three generations (30%).

The family office is a truly bespoke, multi-faceted, often emotionally charged, multigenerational wealth and legacy management vehicle. It needs to encompass the complexities of large families and family governance, asset protection (including often from the families themselves!), tax minimisation and internalisation or outsourcing decisions.

This is no simple task. With that in mind, let’s look at five decisions you may need to make when setting up your family office.

1. How to Structure Your Family Charter

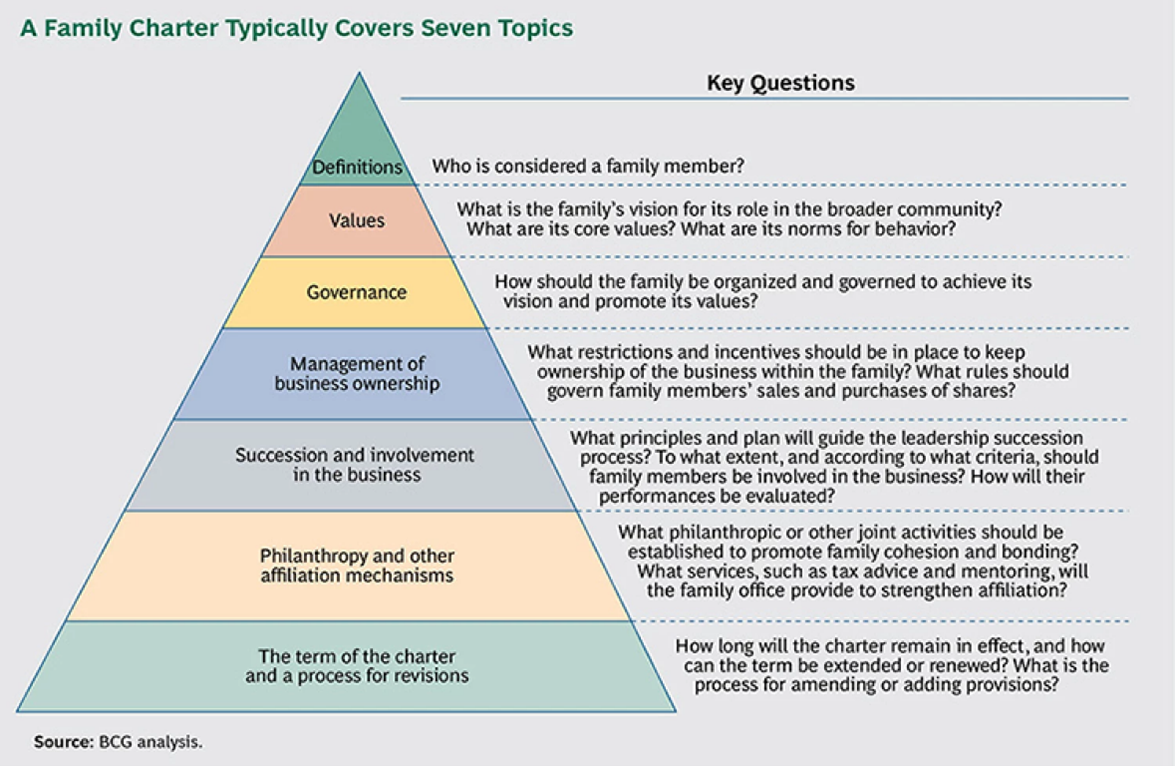

A good starting point is to sit down with your family and write down the family goals, culture and ideals you would like your legacy to achieve. This includes family definitions, values, governance and decision-making, management of family businesses, investment strategy and whether impact or ESG factors play a role. Philanthropy is also an important consideration and can be a good way to involve different family members in the process. Family definitions can be complex and should specifically address the status of current spouses, divorced or widowed spouses, and adopted or extramarital children.

A good charter should be flexible and include a process for an amendment if needed. This chart from Boston Consulting Group outlines the process well:

2. What Assets Will Be Controlled by Your Family Office

Family assets are likely to be extremely wide. They can include cash, family homes, family businesses, investment properties, stocks, bonds, funds, digital, art-work, jewellery and other alternative assets.

It’s important to differentiate between personal use assets and investable assets, although some shared personal use assets—like holiday homes or the super yacht—are often managed by the family offices.

In terms of tax treatment, each class of assets will have specific needs that need to be accounted for. Each tax jurisdiction will also have unique structures that are used to minimise tax legally, so it’s advisable that you speak to a specialised tax adviser.

3. How the Family Business Will Be Handed Over

The family business is often a unique asset that remains at the apex of family affairs. It often continues to be the primary driver of wealth and often legacy.

Family charters may consider whether the family business should remain family owned, or the conditions under which it should be sold. To maintain family ownership families can apply pre-emptive rights to other family members or prohibit sales to some or all investors. Other incentives to maintain family ownership include generous dividend policies or stock loans.

In addition, a family charter should include family members’ roles and responsibilities in running the family business and making business decisions. The charter should describe the capabilities and skills required for executive roles or serving on the board of directors. Conflicts of interest also need to be managed, including market-based remuneration and related party contracts.

4. What Will Be Managed Internally or Externally

Family offices are bespoke. They come in many shapes and sizes, depending on the size of the family’s wealth, the complexity of the family’s affairs, the level of financial sophistication of family members and the family’s lifestyle choices.

Consider what services you wish to internalise or outsource, including:

Family governance

Cashflow forecasting

Tax services

Legal services

Wealth management and asset allocation

Property management

Charitable giving

Wealth succession

Investment education for the family’s next generations

Establishment and operations of private foundations

In general, the larger the family’s wealth and the more complex the family’s affairs, the more sense it makes to hire a professional family office staff. Historically, the mooted scale required to even consider setting up a family office was more than $50m in liquid wealth. There are family office advisers (like Aura Group) who advise and represent multiple family offices (MFOs) to leverage economies of scale by sharing costs.

In an era of digitisation, we believe the next generation of family office offerings will become more accessible to a wider tier of high-net-worth individuals. This new phase will be powered by the adoption of technology and using cloud-based solutions or artificial intelligence to streamline and automate parts of the service offerings and operations.

5. How the Family Office Will Be Structured

Family office structuring includes both considerations of legal structure and governance structure.

It is important to consult both legal and tax advisers on asset protection and structures that minimise tax. Some common legal structures used by family offices include:

Trusts

Insurance Wrappers

Private Corporations

Self-managed pension accounts or funds

Foundations

The family charter should outline clear governance and management structures including:

Trustees

Boards of Directors

Executive leadership ie CEO / CIO

Investment Committee

Other specific sub-committees for example for philanthropic activities

Family Council

The Family Charter should outline the duties and responsibilities of each of these roles and how members are selected or elected.

The creation of a family office is often a great opportunity to revisit and harness the purpose, goals and direction for a family that has amassed wealth and would like to see that wealth protected and retained in the family unit.

Learn more

Aura Group has been developing its family office service offering to be able to cater to the next generation of global wealth. For more information contact us.

Important information

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Group and related entities and is only for information and general news purposes. It does not constitute an offer or invitation of any sort in any jurisdiction. Moreover, the information in this document will not affect Aura Group’s investment strategy for any funds in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Aura Group makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this information. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. You should not construe any such information or any material, as legal, tax, investment, financial, or other advice. This information is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The information may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This information is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in any way.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia.

Family offices sit at the intersection of wealth and legacy. But without a clear framework, even the most successful families can struggle to manage...