Investors continue to try and assess the route of inflation.

While most market participants expect prices to increase as the global economy recovers, concerns about the speed and trajectory of the recent rises persist. In the US, the US Federal Reserve officials continue to downplay rising price pressures as transitory that will quickly fade with post-pandemic normalisation.

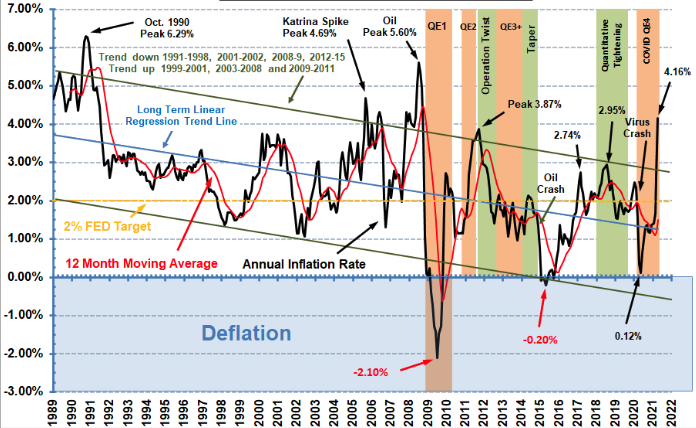

Annual Inflation Rate 1989 - Present

Source: www.inflationdata.com 5/12/2021

US Fed Vice Chair Richard Clarida said the central bank can also take steps to cool a jump in inflation, if it occurs, without derailing the economic rebound coming out of the coronavirus pandemic.

Many commentators believe the US Fed has its head in the sand pointing out that the growth rate of M4 (broad money supply measure) has skyrocketed, growing at 28.9% at the end of 2020, the highest year-end rate since 1943 and today are still elevated at 24%. These rates dramatically exceed a rate that would be consistent with the Fed’s inflation target1.

Deutsche Bank analysts point out that US inflation data surprises are at their highest in 20 years and the last 10 data points were almost off the charts. The consistent data surprises are somewhat inconsistent with the argument that this bout of inflation is transitory2.

Why is inflation so bad for the markets?

When inflation rises, the purchasing value of money declines, and each dollar can buy fewer goods and services. Bond prices tend to fall and stocks become less attractive as it's harder for interest and dividends to keep up with inflation levels. Despite finding it harder to keep up with inflation levels, dividend-growing stocks do offer a hedge against inflation.

The purchasing power of people declines: As wages increase due to inflation, taxation on income increases due to tax bracket creep, leaving people with less money in their pocket to pay for more expensive goods. This phenomenon amplifies the negative effects on consumers and investors, who now have less money to invest

Inflation can be self-perpetuating as it may cause future inflation expectations to rise. For example, an increase in inflation causes people to demand higher wages which itself translates to higher inflation.

Central banks tend (ordinarily) to use monetary policy to cool inflation, by raising the cost of borrowing. This can also have a negative effect on bond and stock prices, in particular growth stocks whose cashflows need to be discounted from way into the future.

The Great Inflation in the 1970s.

The worst stock performance of the 1970s came not when inflation peaked but when it first spiked rapidly. From 1972 to 1973, inflation doubled to more than 6 percent. By 1974 it was 11 percent. In those two years, the S&P 500 declined by a combined 40 percent. Inflation was higher in 1979 and 1980, topping out at 13.5 percent, by which time the S&P 500 had long returned to positive performance, though on an inflation-adjusted base. It was a lost decade for stocks3.

Investing during Inflationary Periods

In the late 1970s and early 1980s, Warren Buffet devoted significant portions of the Berkshire Hathaway annual letter to investing in stocks during inflationary periods3.

“Unfortunately, earnings reported in corporate financial statements are no longer the dominant variable that determines whether there are any real earnings for you, the owner. For only gains in purchasing power represent real earnings on investment. If you (a) forego 10 hamburgers to purchase an investment; (b) receive dividends which, after tax, buy two hamburgers; and (c) receive, upon sale of your holdings, after-tax proceeds that will buy eight hamburgers, then (d) you have had no real income from your investment, no matter how much it appreciated in dollars. You may feel richer, but you won’t eat richer.”

“High rates of inflation create a tax on capital that makes much corporate investment unwise - at least if measured by the criterion of a positive real investment return to owners.”

Warren’s advice is to look for companies that are generating cash, can increase prices inelastically and handle a lot more business without having to incur a lot of capital expenditure. This is probably great advice irrespective of the inflationary cycle.

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Group and related entities and is only for information and general news purposes. It does not constitute an offer or invitation of any sort in any jurisdiction. Moreover, the information in this document will not affect Aura Group’s investment strategy for any funds in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Aura Group makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this information. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. You should not construe any such information or any material, as legal, tax, investment, financial, or other advice. This information is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The information may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This information is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in any way.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia.

What products are typically considered to be illiquid? Examples often cited are private credit, private equity, venture capital, hedge funds and some...

Tong Hoe Sng

Nov 4, 2024

Get the Latest News & Insights from Aura Group

Subscribe to News & Insights to stay up to date with all things Aura Group.