Whilst recessions are costly, they are argued to be the natural balancing act needed to end the misallocation of investment capital when bubbles occur.

A recession is commonly defined as two or more quarters of consecutive negative economic growth. Recessions are often characterised by growing unemployment and bankruptcies, as demand slows from businesses and consumers.

Whilst recessions are costly, they are argued to be the natural balancing act needed to end the misallocation of investment capital when bubbles occur.

Our current situation is very different to 2008, which was caused by lending excesses in the US housing market or the pandemic-related collapse of 2020. Today we need to grapple with many more factors at play which could cause a recession, such as:

• The continued impacts of the pandemic on demand (China is still enacting a COVID-zero policy) and supply chains;

• The Ukraine War and global political unrest; and

• The soaring cost of energy and food.

Combined with loose monetary and fiscal policy this has caused both demand-driven inflation and supply-driven inflation, which will be harder to contain with interest rate rises and quantitative tightening.

With inflation already eating into the consumer’s hip pocket the possibility of mortgage rates doubling (or more) could only further negatively impact discretionary spending. A similar story applies to a reduction in available credit.

Deflating asset prices, especially in the technology and cryptocurrency sectors, is adding to the pain. Many retail investors entered the market only in the last few years and are now nursing heavy losses. Because these sectors include many unprofitable businesses that will now find it tough to raise further capital, layoffs are rising fast with many bankruptcies likely to follow. Even profitable businesses are now more focussed on cost optimisation, leading to the efficient allocation of capital—that tech guy you’ve been trying to hire likely has gotten cheaper!

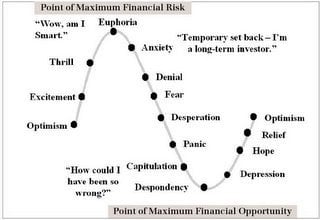

With negative sentiment and asset prices falling, intense emotions often impair rational decision-making. The below is a commonly used market psychology cycle that seeks to explain how emotions evolve and the effect they have on our investing decisions.

It's important to understand that the most opportune time to invest for the long term is when it feels the most uncomfortable, that is when the rest of the market is experiencing fear, desperation, panic and capitulation. It’s a fool’s game to try and time the bottom. This can be true of both business expenditures (hire that resource!) and financial investments. In the June quarter, we’ve made three new hires at Aura and are preparing to deploy more capital whilst assets are on sale.

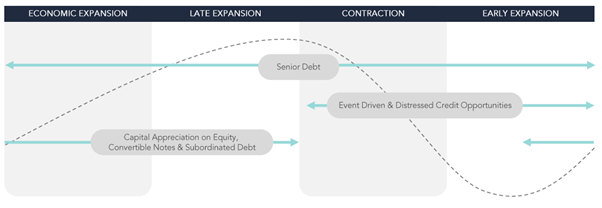

At Aura Group, our Tactical Opportunities Strategy was designed exactly to take advantage of these market cycles. The Strategy’s wide mandate allows investors to rotate between debt and equity securities depending on the market cycle.

Over the next 6-12 months, we intend to shift from short-duration private credit that has performed well to increase our equity exposure via convertibles or beaten-down listed equities. We are finding individual stocks with growing earnings, trading at PE’s 5-10x with fully franked dividend yields of 5-10% pa. We also like names that are executing share buybacks, which have insiders buying and generating potential near-term value catalysts like M&A activity.

It has been 13 years since the last real bear market (April 2020 didn’t last long enough), so it may be wise to take advantage of this one while it lasts.

Important information

This information is provided by Aura Group and related entities and is only for information and general news purposes and does not constitute any offer or any such invitation of any sort or in any jurisdiction. You should not construe any such information or any material as legal, tax, investment, financial, or other advice. This email is intended for distribution only in those jurisdictions and to those persons where and to whom it may be lawfully distributed. All information is of a general nature and does not address the personal circumstances of any particular individual or entity. None of the information constitutes professional and/or financial advice, nor does any information constitute a comprehensive or complete statement of the matters discussed. The views and opinions expressed in this material are those of the author as of the date indicated and any such views are subject to change at any time based upon market or other conditions. The email may contain certain statements deemed to be forward-looking statements, including statements that address results or developments that Aura expects or anticipates may occur in the future. Any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected in the forward-looking statements. This email is for the use of only those persons to whom it is given. If you are not the intended recipient, you must not disclose, redistribute or use the information in this email in any way. If you received it in error, please tell us immediately by return email and delete the document.

Aura Group subsidiaries issuing this information include Aura Group (Singapore) Pte Ltd (Registration No. 201537140R) which is regulated by the Monetary Authority of Singapore as a holder of a Capital Markets Services Licence, and Aura Capital Pty Ltd (ACN 143 700 887) Australian Financial Services Licence 366230 holder in Australia and is issued to accredited, qualified, wholesale, sophisticated and institutional investors only. This email only relates to general news and information only and should not be construed as an offer.